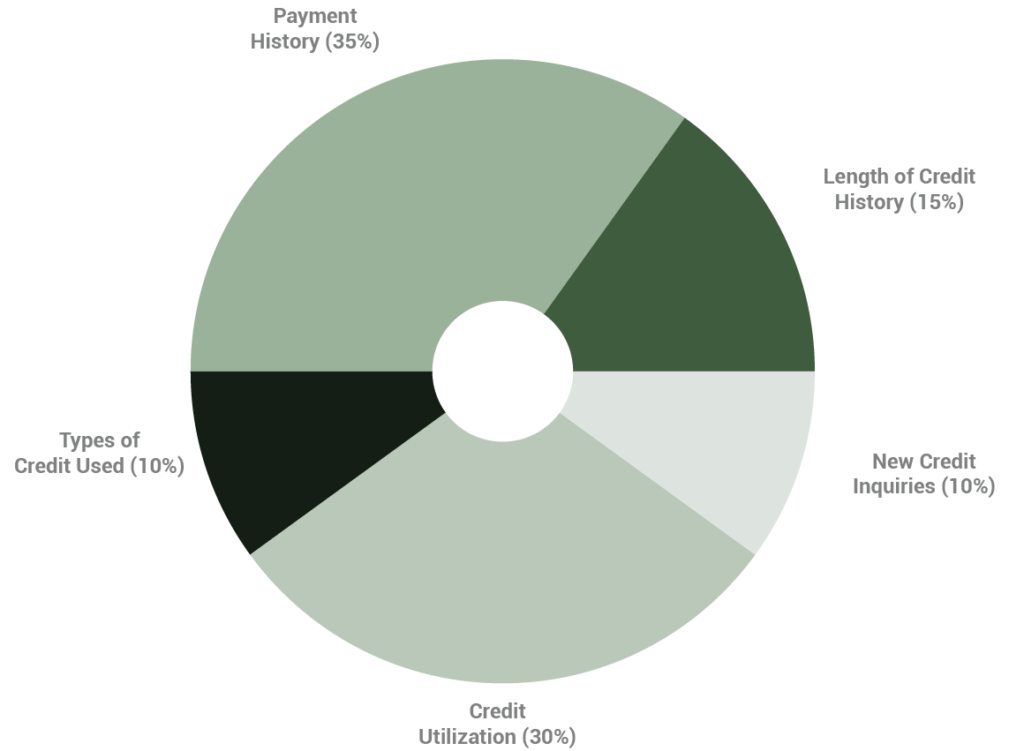

These five factors play a crucial role in determining your credit score. Understanding and working to improve them

is a key part of getting your credit ready for homeownership.

Payment History (35%)

This is the most important factor.

Lenders want to know if you’ve

paid your past credit accounts

on time. Late payments, defaults,

bankruptcies, and collections can

significantly lower your score.

Maintaining a history of

on-time payments helps

demonstrate your reliability as a

borrower.

Credit Utilization (30%)

Credit utilization refers to the

ratio of your current credit card

balances to your credit limits. A

high balance compared to your

credit limit can negatively impact

your score. Keeping your credit

utilization below 30% is a good

goal for improving your score.

Length of Credit History (15%)

The length of time you’ve had

credit accounts affects your score.

A longer credit history shows

lenders that you have experience

managing credit. If you’re new to

credit, you may want to focus on

building a positive credit history

before applying for a mortgage.

Types of Credit Used (10%)

This factor looks at the variety of

credit accounts you have—such

as credit cards, mortgages, and

auto loans. A healthy mix of credit

accounts can improve your score,

but it’s not necessary to open

multiple accounts just to boost

your score. Quality over quantity

is key.

New Credit Inquiries (10%)

Every time you apply for new

credit, a “hard inquiry” is made,

which can slightly lower your

score. Frequent credit inquiries

within a short period suggest a

higher risk to lenders. It’s wise to

limit credit applications, especially

when you’re planning to apply for

a mortgage.

Ready to Improve Your Credit?

By following these tips, you can take control of

your credit score and move closer to your goal of

homeownership. If you’re looking for more in-depth

strategies to boost your score and clear up negative

marks, check out our Credit Cleanup Guide, designed to

help you achieve a cleaner, healthier credit report.

1. Borrow only what you can afford to repay

Taking on more debt than you can manage will hurt your

credit score and make payments difficult.

2. Make all of your payments on time

Timely payments are the most important factor in your credit score.

Set reminders or automate payments to stay on track.

3. Avoid excessive credit inquiries

Too many credit checks in a short period can lower your score. Be

strategic with credit applications, especially when preparing for a

mortgage.

4. Create an emergency fund

Having an emergency account to cover unexpected expenses can

prevent you from relying on credit and missing payments.

5. Review your credit report regularly

Check your credit report at least once a year to spot errors. Dispute

any inaccuracies to ensure your score isn’t unfairly impacted.

6. Keep a low credit utilization ratio

Aim for a credit utilization of less than 30%. The lower your balance

relative to your credit limit, the better it is for your score.

7. Avoid opening new store credit cards

Store credit cards might offer instant savings, but they can lower

your score and increase your financial stress in the long run. A small

discount now isn’t worth the potential cost on a larger loan.

8. Don’t shy away from using credit

To build a score, you need to use credit. Just be sure to use it

responsibly, paying off your balances in full each month when

possible.

9. Maintain a mix of credit types

A combination of revolving (credit cards), installment (auto loans,

mortgages), and secured accounts can positively influence your score.

However, don’t open unnecessary accounts just for variety.